Community benefit is a well-defined set of activities articulated by the Internal Revenue Service. The IRS has identified specific categories of community benefit with detailed definitions and specific accounting guidelines. The IRS requires that to be reported, a community benefit must respond to an identified community need and meet a community benefit objective, such as improving community health, increasing access to health services, enhancing public health, educating health professionals, or relieving the government burden to improve health.

Integral to the mission of Catholic and other not-for-profit health care organizations, community benefit is an extension of not-for-profit hospitals' historic mission to meet the needs of the time in their communities, especially the needs of vulnerable and disenfranchised members in their communities.

2025 Updated Version

Community Benefit Guide

CHA's A Guide for Planning & Reporting Community Benefit provides a comprehensive framework for nonprofit health care organizations to develop and strengthen their strategic approach to assessing. planning, implementing and reporting community benefit.

Recommended Resources

More Resources

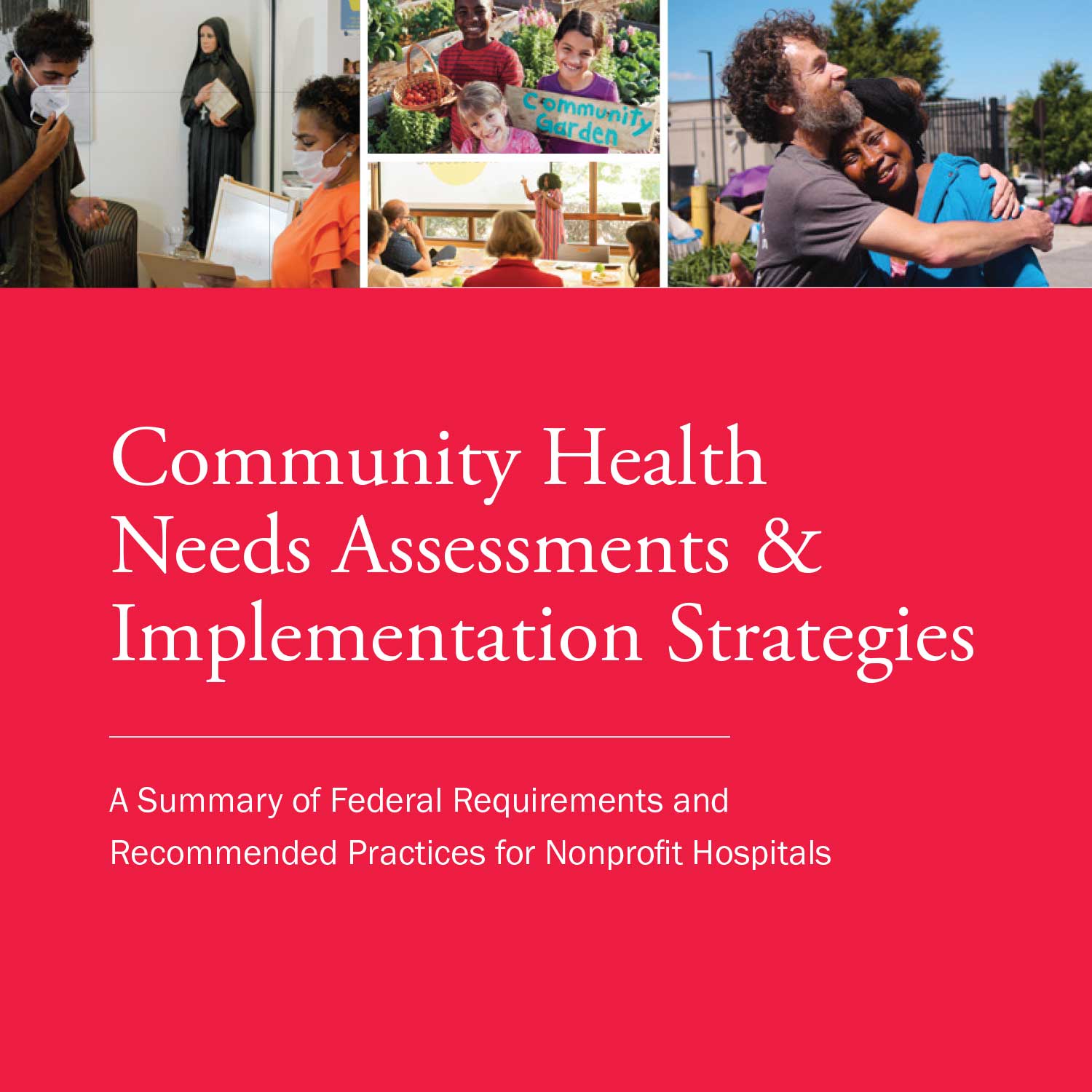

Community Health Needs Assessments & Implementation Strategies: A Summary of Federal Requirements and Recommended Practices for Nonprofit Hospitals

This booklet provides a concise overview of federal requirements for tax-exempt hospitals to conduct and adopt community health needs assessments (CHNAs) and implement strategies to address identified needs. It reflects the IRS's final rules, issued on December 31, 2014, in IRC Section 501(r)(3), and includes recommendations from community benefit and public health experts. This resource can be used to educate internal and external stakeholders who play a vital role in supporting the hospital’s assessment and community health improvement planning efforts, such as hospital trustees, finance and marketing staff, local health departments, and social service organizations.

Community Benefit Reporting Resources

This new set of resources was developed to help tax-exempt hospitals more accurately report their community benefit expenses. Designed for finance/tax staff, they can also help community benefit professionals better understand how they can support their finance/tax colleagues do this work.

.jpg?sfvrsn=b0c7b00b_1)

Investing in Community Health: A Toolkit for Hospitals

This toolkit is designed to help health care organizations look at their resources in a different light, expand their efforts to support their communities, and maximize their impact on community health by harnessing the power of their investment capital.

.jpg?sfvrsn=26caa26_1)

Healing the Multitudes - Catholic Health Care's Commitment to Community Health - A Resource for Boards

This resource, Healing the Multitudes – Catholic Health Care’s Commitment to Community Health: A Resource for Boards, explains why the Catholic health ministry is called to take a leadership role in addressing the social determinants of health and the board’s key role in making this work a strategic focus of their organization. This focus on addressing the root causes of poor health is not unique to Catholic health care. What is unique to Catholic health care is that our faith compels us to give special attention to our neighbors who are economically poor and to work for the common good. It is these values that drive us to lead the way in this work, even when the path forward is not clear.

Evaluating Your Community Benefit Impact

It is essential to evaluate community benefit programs in order to improve programs and ensure the effectiveness of actions taken to address significant health needs in the community.Community benefit program evaluation is important for compliance reasons as well. The Affordable Care Act added requirements for tax-exempt hospitals to assess the health needs of their communities every three years. The federal regulations implementing those requirements specify that hospitals need to include in their community health needs assessment (CHNA) reports an evaluation of the impact of actions taken to address the significant health needs from their immediately preceding CHNA report (Treas. Reg. § 1.501(r)-3). The intent of these requirements is to increase transparency and accountability around tax-exempt hospitals' obligation to improve community health.This CHA resource, developed in collaboration with Vizient and the Healthy Communities Institute, is designed to help community benefit leaders take a systematic approach to evaluating and improving their programs and to meet their legal requirements by applying the knowledge and experience of public health program evaluation to community benefit programs.While the resource is primarily geared to staff members who work in the area of community benefit, it can also be used by others who need to understand how to assess evaluation findings and use those findings in their work. Other groups that may find this information useful include trustees; executive leaders; strategy; population health; finance and communications staff; community partners; and program participants.Members Only: View and download a copy of Assessing and Addressing Community Health Needs. (Note: you must be logged in to access)

Assessing and Addressing Community Health Needs

Responding to the health needs of our communities, especially to the most vulnerable among us, is central to the mission of Catholic and other not-for-profit health care organizations. To do so, we need to have an understanding of community health needs and use a deliberate approach for addressing those needs.The importance of assessing community health needs and developing an implementation strategy to address selected needs was reinforced by the Patient Protection and Affordable Care Act (Affordable Care Act), enacted March 23, 2010. The law added new requirements on tax-exempt hospitals to conduct community health needs assessments and to adopt implementation strategies to meet the community health needs identified through the assessments.CHA, in collaboration with Vizient and the Healthy Communities Institute, developed this resource to help not-for-profit health care organizations strengthen their assessment and community benefit planning processes. Using CHA’s previous work, the experience of community benefit professionals and public health expertise, this resource offers practical advice on how hospitals can work with community and public health partners to assess community health needs and develop effective strategies for improving health in our communities.This resource was developed especially for the hospital staff responsible for conducting or overseeing community health needs assessments and planning community benefit programs.Others with an interest in community health may find this book useful as well. These could include staff within the organization such as administrators, clinicians and strategic planners, and community partners such as policy makers, consumer advocates, public officials and representatives of community groups.Members Only: View and download a copy of Assessing and Addressing Community Health Needs. (Note: you must be logged in to access)https://www.chausa.org/docs/default-source/member-only/focus-areas/community-benefit/community-benefit-assessing-and-addressing-full-book.pdf

CHA Articles

-

April 2026CHI Mercy Health's foundation annually hosts a filmmaking project to help prevent violence and other threats.

April 2026CHI Mercy Health's foundation annually hosts a filmmaking project to help prevent violence and other threats. -

March 2026

March 2026SSM Health partners to connect Central Missouri patients who lack transportation with volunteer drivers

The program addresses a key social determinant of health. -

February 2026

February 2026Trinity Health prioritizes nutrition, using clinical and social care strategies to promote food security

Trinity Health works with community partners to impact social influencers of health. -

February 2026

February 2026PeaceHealth's new leader looks to build deeper connections, ensure system's health

As she settles into her new role as president and CEO of PeaceHealth, Sarah Ness sees financial challenges but also a bright future for the system. -

January 2026

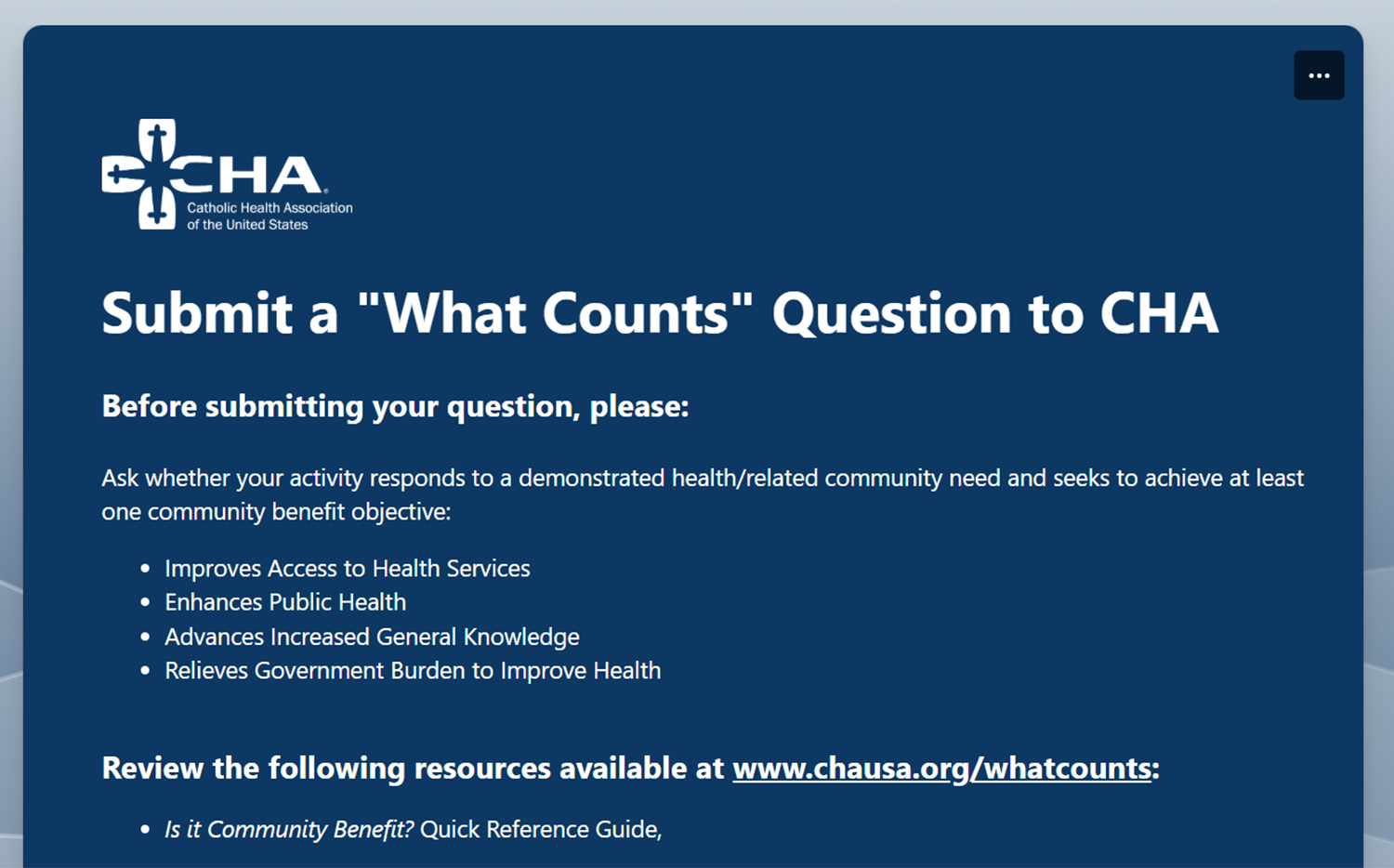

January 2026New button on CHA website streamlines process to get answers on community benefit

The button went live in January. It is one of many CHA resources to find answers about what counts as community benefit. -

January 2026

January 2026Ascension's chief pharmacy officer is on mission to get medications to those in need

Mike Wascovich says stretching finite resources to the most vulnerable is what the ministry is called to do. -

Spring 2026

Spring 2026Community Benefit — Why the IRS Community Benefit Standard for Tax-Exempt Hospitals Has Endured

Over the past several years, tax-exempt hospitals have faced increasing scrutiny over the level of community benefit they provide. Watchdog groups, researchers, members of Congress and other critics have called for laws requiring hospitals to provide a minimum threshold of community benefit to qualify for tax-exempt status. -

Winter 2026

Winter 2026Community Benefit — How Community Benefit Serves as a Living Expression of Catholic Health's Mission and Commitment

While many in Catholic health care are familiar with our Catholic social teaching and the ways it is embedded in the care that we provide, these Catholic social teachings are also the central tenets of our community benefit programs and activities. -

Fall 2025

Community Benefit - What's the Point of Doing a Needs Assessment and Improvement Plan if They Don't Lead to Real Change?

Community health needs assessments (CHNAs) and community health improvement plans (often known as CHIPs or implementation strategies — same thing!) represent major investments, not just in time and resources, but in the potential for meaningful change. -

Summer 2025

Community Benefit — Nonprofit Hospital Community Benefit: What Counts and Why It Matters

There is only one definition of community benefit: it is the Internal Revenue Service (IRS) definition. Other organizations, researchers and lobbyists, at times, will add or subtract categories to the way they define community benefit... -

Spring 2025

Spring 2025Community Benefit — Navigating Financial Assistance at Mercy: Compassionate Care for Patients

At Mercy, we are committed to delivering compassionate, high-quality care and understand that financial barriers should not prevent anyone from receiving the care they need. Accessing health care can be overwhelming, particularly for individuals and families facing economic difficulties. As part of our mission to bring the healing ministry of Jesus to life, we offer financial assistance programs to try to ensure equitable access to medical services for all. -

Winter 2025

Flourishing Children Benefit All of Us — For Generations to Come

Childhood is a time of growth, learning, wonderment and hope, filled with the potential of a full and prosperous life ahead. Unfortunately, not all children and young people are given the opportunities and support required to flourish and reach their full potential.

Season 6: Episode 6 - Collaborating to Address Food Insecurity in Rural Communities

Health Calls Season 6, Episode 6 focuses on addressing food insecurity in rural communities. Host Brian Reardon and Executive Producer Josh Matejka welcome Lindsey Meyers, MBA, Vice President of Communications, PR, and Community Engagement at Avera Health.

Lindsey shares how Avera’s community health needs assessments revealed rising food insecurity across its largely rural footprint, prompting the creation of wellness pantries within clinics. These pantries provide emergency food supplies and connect patients to sustainable resources, complementing mobile food pantries and partnerships with Feeding South Dakota. Lindsey explains why food access is essential to whole-person care and how collaboration among clinicians, volunteers, and community partners drives success. The conversation highlights the program’s rapid growth, its impact on patients, and underscores Catholic health care’s commitment to meeting social determinants of health and evolving to serve community needs."

Health Calls is available on the following podcast streaming platforms:

Season 5: Episode 9 - Data 101 for Community Benefit

When it comes to learning about and treating the communities we serve, data is the key. But with so much data out there, how do Catholic health providers begin to sort through it all and make sense of what they find?

Jaime Dircksen, Vice President of Community Health and Well-Being at Trinity Health, joins the show to discuss how she and her team utilize data to best serve Trinity Health's patient populations. She discusses key indicators they look for, how different customizable tools can help or harm the process and how generative AI and emerging technologies offer hope and caution to caregivers looking to better connect with their patients.

Resources:

- Read Dircksen's recent article in Health Progress, "New Ways to Measure Impact in Communities"

- Purchase or download CHA's A Guide for Planning and Reporting Community Benefit

- Plan to attend Community Benefit 101, CHA's vital annual program which provides the basics of community benefit programming

- Transcript